Middle East conflict pushes aluminium to 4-year high; more upside seen

- Aluminium prices hit fresh highs on conflict-driven supply fears.

- GCC smelters are vulnerable due to heavy dependence on imported raw materials.

- The ultimate price movement depends on duration of disruption at Strait of Hormuz.

The escalating conflict in the Middle East is now driving significant upside risks for aluminium prices and physical premiums.

The central question for the market has shifted from the mere threat to the Strait of Hormuz to forecasting the potential duration of supply disruptions, according to an ING Group report.

Iran's Supreme Leader, Ayatollah Ali Khamenei, was killed in US-Israeli airstrikes over the weekend, leading to immediate Iranian retaliation across the region.

This escalation has severely impacted energy and industrial activity, most notably by impairing shipping through the critical Strait of Hormuz.

Initial market impact and price surge

The initial effects of the situation are already evident.

Qatalum, a joint venture between Qatar's state-owned aluminium producer and Norsk Hydro, initiated a controlled halt in production on Tuesday.

The company, which has a primary aluminium capacity of 636 kilotonnes (kt), indicated that a complete resumption of operations could require six to twelve months.

Furthermore, Hydro has issued a force majeure notice to Qatalum's clientele.

Following Iranian attacks that necessitated the shutdown of QatarEnergy's major LNG plant, the company announced a halt in aluminium and certain chemical production.

This development initially caused aluminium prices to surge by as much as 3.8% to reach $3,315 per ton.

On Wednesday, prices hit a nearly four-year high of $3,418 per ton on the London Metal Exchange.

The UAE's largest aluminium producer, Emirates Global Aluminium, has indicated that it is using offshore inventories as a way to handle delays in loading.

GCC's structural vulnerability and global exposure

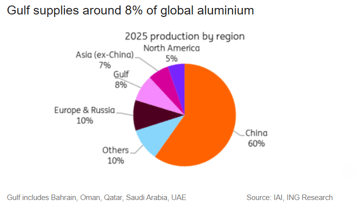

The Gulf Cooperation Council (GCC), comprising Bahrain, Oman, Qatar, Saudi Arabia, Kuwait and the UAE, faces a structural vulnerability in its aluminium industry.

While the region contributes approximately 8% of the world's aluminium output, its production of key raw materials is significantly lower—around 3% for alumina and just 1% for bauxite.

This stark contrast makes the GCC's aluminium smelters heavily dependent on raw material imports, ING Group said in the report.

The limited storability of alumina compromises resilience.

Although smelters generally maintain alumina inventories sufficient for three to four weeks—offering a buffer against minor interruptions—extended supply constraints would rapidly escalate into a significant production threat.

“Extended disruption in the Strait would simultaneously choke alumina inflows and aluminium exports for Middle Eastern smelters. That would tighten global supply meaningfully,” Ewa Manthey, commodity strategist at ING Group, said in the report.

Europe is especially vulnerable, as roughly 30% of its aluminium imports come from the UAE.

This dominance makes European premiums particularly susceptible to fluctuations, especially considering the current scarcity of primary aluminium.

The US also faces exposure, as the region accounts for over 20% of its imports. However, the immediate increase in prices is limited by tariff-inflated Midwest premiums.

“Physical premiums in Europe and the US have already repriced to reflect constrained Gulf exports and buyers are accelerating withdrawals from exchange and private warehouses to cover near term needs,” Neil Welsh, head of metals at Britannia Global Markets, said in an emailed statement.

“Middle Eastern smelters account for a material share of seaborne exports and many operate with only a few weeks of alumina feedstock on site, so even short-duration shipping interruptions can force curtailments that amplify tightness across the global chain.”

Already a tight market

The aluminium market was already tight—a perspective we consistently maintained—even before the current shock.

ING’s pre-conflict analysis for 2026 had already projected a deficit of approximately 600kt.

Supply was already constrained by China’s capacity cap, trade disruptions, and the impending shutdown of Mozal.

Supply constraints were already evident due to China's capacity cap, trade disruptions, and the impending closure of Mozal.

Physical market indicators had been strengthening even before the conflict: LME inventories have been decreasing since late last year, premiums are high, and the cash-to-three-month spread has narrowed.

This trend was further highlighted on Tuesday when orders for LME warehouse metal, particularly Malaysian material, reached their highest level since September.

High energy costs

Increased energy prices introduce an additional upward risk through rising cost curves.

Conversely, the primary mitigating risk is demand: an extended conflict could ultimately depress industrial activity and lead to demand destruction.

For metals more broadly, this creates a tension between geopolitical risk premia and weaker end‑use demand.

For aluminium, the balance of risks is currently weighted toward price increases, especially if the disruption at the Strait of Hormuz lasts for a significant period.

The ultimate movement in prices and premiums will be determined more by the duration of the disruption than by its degree of escalation alone.

“We remain bullish on aluminium as supply tightens, with China’s capacity cap, the Mozal shutdown, stalled restarts in Europe and the US, and Middle East disruptions all reinforcing market tightness,” Manthey noted.

Gold prices edge higher despite stronger dollar and treasury yields

Oil prices fall 3% but remain on track for biggest weekly gains in months

Silver price rebounds from sharp losses as markets assess Fed policy

Gold falls despite war risks: has $100 oil rewritten the safe-haven trade?

Brent crude retreats, but a 14% weekly jump says the danger is not fading

No results found

Loading articles...

Failed to load articles. Please try again.