Europe’s fuel supply resilient but fragile as Middle East flows collapse

AI Sentiment: 22/100 Bearish

This score is generated through AI-driven analysis of the article's content.

powered by

Buy SHEL or BP. The article shows Europe running harder: refining margins surged (jet +180%, diesel +170%) and inventories are tightening, so refiners with scale and flexible feedstock access should capture high crack spreads while maintenance is deferred. This is a direct earnings tailwind from the supply squeeze and stock draw, not just a one-off headline.

Key Risk: Refineries are forced to complete deferred maintenance sooner than expected, cutting throughput right when inventories are already low and margins mean-revert.

Sell US refiners/exporters most exposed to Europe crack arbitrage—e.g., Valero (VLO) and Phillips 66 (PSX). Europe’s balance depends heavily on US flows (18% of diesel/jet imports; 22% of crude). If US refinery utilization stays near 98% and domestic demand remains strong, exports can shrink, compressing the export-driven margin that benefits these names.

Key Risk: US exports to Europe don’t fall—either because US runs ease or domestic demand weakens—so the export squeeze thesis fails.

- Imports from Middle East plunge to lowest in a decade after Hormuz closure.

- Europe offsets losses with US and West African flows.

- Analyst warns deferred maintenance and thinning inventories could cut output.

Europe’s transport fuel supply has shown remarkable resilience in the face of the Strait of Hormuz closure, but analysts caution that the balance is fragile and risks are mounting.

A new report from Vortexa highlights how the continent has managed to offset the loss of Middle Eastern barrels through higher imports from the US and West Africa, stronger refining runs, and stock draws.

Middle East flows collapse

Between January 2023 and February 2026, countries in the Middle East Gulf accounted for about 30% of Europe’s seaborne imports of jet fuel and diesel, and roughly 10% of its crude oil and condensate imports, according to data from Vortexa.

The disruption of flows through the Strait of Hormuz has significantly altered those trade patterns.

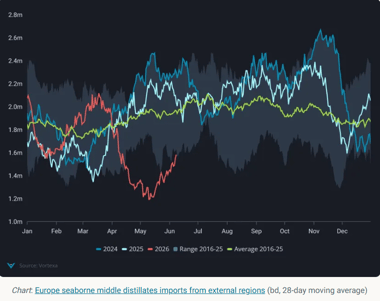

In May 2026, Europe’s imports of middle distillates from the region fell to just 40,000 barrels per day, the lowest level in Vortexa’s 10-year dataset and a decline of 540,000 barrels per day from a year earlier.

West Africa has emerged as an alternative source of supply, with exports to Europe doubling year-on-year to 125,000 barrels per day. Most of that increase came from jet fuel shipments produced by Dangote Refinery in Nigeria.

The United States has also increased exports to Europe.

Shipments from the Gulf Coast rose between 60% and 70% year-on-year in April and May, while exports from the Atlantic Coast reached a record 110,000 barrels per day in April, led primarily by diesel.

Despite these replacement flows, Europe’s overall seaborne fuel imports remain significantly below year-ago levels, with diesel imports down about 20% and jet fuel imports down roughly 50% in May.

Refining runs and stock draws

Europe’s domestic refining sector has helped offset some of the disruption to fuel supplies.

Seaborne crude imports averaged about 11.5 million barrels per day between March and May, up from 11 million barrels per day during the same period a year earlier.

Higher imports from the United States Gulf of Mexico region, Norway, and CPC Blend producers helped compensate for reduced inflows from the Middle East.

However, inventories have been tightening. Crude stockpiles have fallen by approximately 12.9 million barrels since April, leaving inventories at seasonally low levels.

Refiners have responded to strong profit margins by maximising output.

In Northwest Europe, refining margins have risen sharply, with gasoline cracks up about 35%, jet fuel margins up 180%, and diesel margins up 170%.

To capture these favourable economics, many operators have deferred maintenance work, reducing offline refining capacity to roughly half of last year’s level.

While this has helped sustain supply in the near term, the approach is unlikely to be sustainable indefinitely.

Deferred maintenance will eventually need to be completed, potentially reducing refinery throughput at a time when both crude and refined-product inventories are already relatively low.

Demand shifts and risks ahead

Signs of demand moderation are emerging. Eurozone automotive fuel sales fell 3.5% year-on-year in April, the steepest drop since October 2023, the data showed.

The UK saw a sharper 10% decline despite subsidies and tax cuts. Jet fuel demand, however, remains resilient.

Eurocontrol data shows flight traffic up 0.7% year-on-year in June, keeping jet inventories under pressure.

Stocks in the Amsterdam-Rotterdam-Antwerp hub fell 39% year-on-year, their lowest since 2020. Diesel inventories are also down 10% year-on-year.

Europe’s balance now depends heavily on US flows. In May, 18% of Europe’s diesel and jet imports and 22% of crude imports came from the US, but with American refinery runs near 98% utilization and domestic demand strong, exports could shrink.

US Gulf Coast crude inventories are already down 6% month-on-month.

Turkey could emerge as a relief valve, with its crude imports from non-Russian sources up 390,000 barrels per day year-on-year.

This may allow more refined products to flow into Europe, given the EU ban on Russian distillates.

Ernest Censier, market analyst at Vortexa, summed up the situation

Europe’s transport fuels supply is resilient but vulnerable. The continent has managed to offset the loss of Middle Eastern barrels through higher imports from the US and West Africa, stronger refining runs and stock draws. However, the balance is fragile and risks loom large as inventories thin and deferred maintenance could cut refinery output later this year.

The outlook is clear as Europe has managed to keep fuel flowing, but the system is stretched.

If US exports falter or European refineries undergo delayed maintenance, the buffer could vanish quickly.

For now, resilience masks vulnerability, but the coming months may test just how thin that margin really is.

Gold price tops $4,040: is a fresh run toward $4,100 now taking shape?

Brent crude price analysis: Is the market being too complacent?

Top professor explains why WTI crude oil price could surge soon

Silver price rebound turns dangerous as $57.50 resistance hardens

Gold price nears breaking point as Fed fears threaten brutal collapse

No results found

Loading articles...

Failed to load articles. Please try again.