Oil and gas prices underpricing Hormuz risks warns ING

AI Sentiment: 78/100 Bullish

This score is generated through AI-driven analysis of the article's content.

powered by

Buy ICE Brent crude futures (front-month into 3Q26, or a 3Q26/4Q26 calendar spread). ING flags underpricing of prolonged Hormuz inhibition through end-July, with a 3Q26 deficit and a base case of ~$110 and upside spikes to $120–130 if no late-July resolution. The setup is a classic “calm market before the inventory math breaks,” especially as summer demand hits and buffers thin.

Key Risk: A quick US-Iran deal that restores flows before late July, collapsing the deficit and taking Brent back below $100.

Buy TTF natural gas futures (front-month/near-curve). ING sees Europe also underpricing risk: LNG exports down >7% YoY, storage only ~43% full (below the 5-year average), and limited incentive to inject due to the forward curve. If Persian Gulf disruptions persist, Asia competes harder for spot LNG and Europe faces a winter-prep squeeze—driving sharp near-term upside.

Key Risk: A sustained build in European storage (or a major LNG supply reroute) that removes the winter-prep fear and pushes TTF back toward the forward curve.

- Markets complacent despite major supply shock from Hormuz.

- ING expects flows inhibited until end of July.

- Brent to average $110/bbl in 3Q26 with upside risks.

Energy markets are showing signs of complacency in the face of a major supply shock caused by the ongoing closure of the Strait of Hormuz, according to ING Economics.

Despite three months of restricted flows and little tangible progress in US-Iran negotiations, oil and gas prices have failed to fully price in the severity and potential duration of the disruptions.

Brent crude continues to hover below the psychologically important $100 per barrel level, while European gas prices have also remained relatively stable.

This muted reaction comes even as visible commercial traffic through the world’s most critical energy chokepoint has collapsed.

Analysts warn that current price levels may be underestimating the risks, especially as seasonal summer demand approaches and inventory buffers start to thin.

Limited visible flows but market calm persists

With little tangible evidence of an imminent deal between the US and Iran to resume energy flows through the Strait of Hormuz, ING believes the market is underpricing risks.

Brent crude has remained below $100 per barrel despite the disruption of a significant portion of global oil supply.

Warren Patterson, Head of Commodities Strategy at ING Economics, warned: “With little tangible evidence of an imminent deal between the US and Iran to get energy supplies flowing through the Strait of Hormuz once again, we believe oil and gas markets are being too complacent, and see significant upside in the absence of a quick resolution.”

July inflection point expected

ING’s base case assumes that flows through the Strait will remain largely inhibited until the end of July.

“We are of the view that Strait of Hormuz flows will remain largely inhibited until the end of July,” Patterson said.

This prolonged disruption is expected to leave the oil market in deficit during the third quarter.

ING forecasts Brent averaging $110 per barrel in 3Q26, with potential spikes to $120-130 per barrel if no resolution is reached by late July.

Such a move could increase pressure for a diplomatic breakthrough.

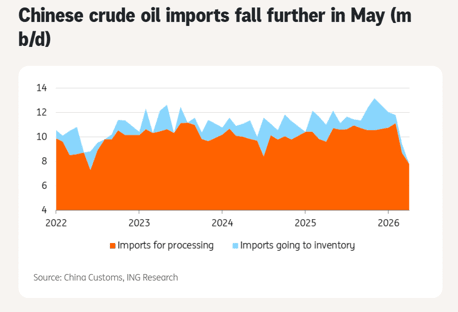

Chinese demand and other buffers provide temporary relief

Falling Chinese oil imports have offered some short-term relief. Crude imports dropped sharply in May to 7.8 million barrels per day, the weakest level since October 2017.

However, Patterson noted uncertainty around how long China can rely on inventories amid the disruption.

Other mitigating factors include increased US exports, strategic reserve releases (which are winding down), and some demand destruction.

These buffers are temporary and may not hold if the crisis extends deeper into the third quarter, when seasonal demand strengthens.

European gas market also vulnerable

The European gas market is similarly underpricing risks. Global LNG exports fell more than 7% year-on-year in May, with Persian Gulf disruptions playing a major role.

While new US LNG capacity has helped partially offset losses, it has not been enough to fully compensate.

European storage levels are currently around 43% full, well below the five-year average. The forward curve offers limited incentive for injection, raising concerns about winter preparedness.

Increased competition from Asia for spot LNG could push prices higher if disruptions persist.

Outlook and risks

ING expects prices to trend lower in 4Q26 and 2027 as flows eventually recover, but near-term upside risks remain prominent.

Without a swift resolution, the combination of depleting buffers, seasonal demand strength, and potential aggressive Asian buying could trigger sharp price increases.

Patterson emphasised the importance of monitoring inventory developments.

From an inventory perspective, we believe that the end of July could be an inflection point for the market if there is no improvement in energy flows from the Persian Gulf.

The analysis highlights how markets are currently relying on temporary mitigations rather than addressing the structural supply gap.

Should negotiations drag on, the risk of a disorderly price spike increases significantly.

For now, the energy complex appears to be in a wait-and-see mode.

However, ING’s analysis suggests this calm may prove deceptive, with the potential for substantial volatility and higher prices if the Hormuz situation remains unresolved through the critical summer months.

Policymakers, traders, and consumers would be wise to prepare for a tighter and more expensive energy environment in the coming quarter.

Brent breaks $92 as a second oil supply shock begins to unfold

Silver price jumps for fourth day as $60 breakout comes into focus

Gold price hits two-week high as Middle East risks revive haven demand

Here’s why wheat prices are soaring this year

Gold price tops $4,040: is a fresh run toward $4,100 now taking shape?

No results found

Loading articles...

Failed to load articles. Please try again.