Here’s why Barclays share price has jumped to a 19-year high

AI Sentiment: 82/100 Bullish

This score is generated through AI-driven analysis of the article's content.

powered by

Buy BARC.L. Catalysts stack: strong investment-banking momentum (equity + debt advisory), trading tailwinds from higher volatility, and a clear shareholder-return plan (buybacks + dividends) alongside upgraded 2028 return-on-tangible-equity guidance (14%). Technicals confirm trend strength: breakout above 506p, ADX ~36.7 (momentum), RSI ~70 (bullish trend). Thesis killer: a sharp drop in deal activity/trading revenues (investment bank fees and market volatility) that forces Barclays to slow or cancel buybacks and guidance.

Key Risk: Investment-banking and trading revenue falls fast enough to force weaker guidance and smaller buybacks.

Buy LLOY.L as a relative-value beneficiary. If Barclays’ outperformance is driven by the whole UK rates + capital-markets cycle, the market will eventually re-rate the laggards. Barclays’ strength also signals investors are paying up for banks with credible capital returns; Lloyds should catch that multiple expansion as guidance and buyback expectations firm up. Thesis killer: Lloyds’ credit quality or capital position deteriorates (rising delinquencies/impairments) and the market stops rewarding UK banks with higher multiples.

Key Risk: Credit losses rise and investors stop believing in sustained capital returns.

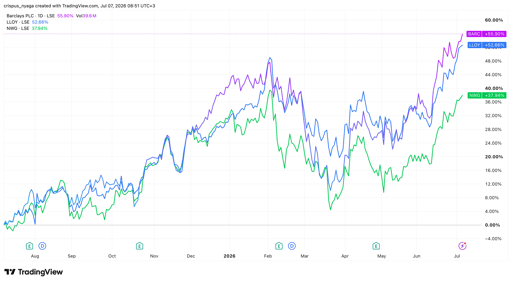

- Barclays shares have soared by 55% in the last 12 months.

- The company’s investment bank is doing well as M&A deals rise.

- Its trading business will likely benefit from the market volatility.

Barclays share price has gone parabolic in the past few months, reaching its highest point since 2007. It has soared by 55% in the last 12 months, outperforming its top peers like Lloyds and NatWest, which have jumped by 52% and 37% in the same period.

Barclays Bank has two key catalysts

Barclays, a top global bank, is doing better than other UK banks because of its business strategy. Unlike NatWest and Lloyds, Barclays has a huge investment bank, whose business is doing well.

WSJ data shows that the bank is among the best in the equity capital market business. It has advised transactions worth over $24 billion this year, higher than the $11 billion it did by this time last year.

Barclays also ranks high in the debt market, where it has advised on deals valued at over $242 billion. By this time last year, it had advised on transactions worth over $220 billion.

WSJ estimates that its investment bank revenue stands at $1.8 billion so far this year, higher than last year’s $1.6 billion.

Barclays may benefit from the ongoing European M&A deals. Schroders was acquired by Nuveen in a $13.4 billion deal, while EasyJet agreed in principle to be bought by Castlelake, an American company. That buyout could trigger more consolidation in Europe’s aviation sector.

At the same time, Barclays’ trading business is expected to remain vibrant this year because of the rising volatility. This volatility was caused by the ongoing AI supercycle and the recent US-Iran war.

Most importantly, its core British business is expected to benefit from the elevated interest rates. The Bank of England (BoE) has left interest rates unchanged at 3.75%, with traders predicting that it will not cut this year. Banks normally benefit in a high interest rate environment because they boost their net interest margin.

Barclays reported strong Q1 numbers

The most recent results showed that Barclays did well in the first quarter, helped by its investment bank, high interest rates, and its trading business. These numbers helped it to initiate a share buyback plan worth £500 million.

Barclays announced a net income of £8.2 billion, with its profit before tax rising to £2.8 billion. Most importantly, it boosted its forward guidance, with its 2028 return on tangible equity rising to 14%. It also expects to return £15 billion to investors through share buybacks and dividends between 2026 and 2028. These are huge numbers for a bank with a market capitalization of £71 billion.

Barclays UK’s revenue grew by 9%, helped by high interest rates and low delinquencies, while its UK corporate bank grew by 10%. Its investment bank and US consumer bank business grew by 4% and 14%, respectively.

Barclays share price technical analysis

Source: TradingView

Technical analysis suggests that Barclays has more room to grow in the near term. It has already jumped above the crucial resistance level of 506p, its highest level since February, confirming that bulls have prevailed. Moving above that level also invalidated the forming double-top pattern.

The Average Directional Index (ADX) has jumped to 36.7, its highest level since January 16. A rising ADX is a sign that an asset is gaining momentum. The same is happening with the Relative Strength Index (RSI), which has jumped to 70.

Therefore, the path of the least resistance for the shares is upward, with the next key target to watch being at 550p.

Why are Micron, Sandisk, and SK Hynix stocks falling today?

Strategy stock jumps as Bitcoin buying pause enters fifth straight week

What Intel earnings tell us to expect from AMD next week

D-Wave stock is soaring and it's not entirely about AT&T partnership

ASML stock sinks as China reportedly starts producing homegrown DUV chip machines

No results found

Loading articles...

Failed to load articles. Please try again.