Amazon stock is struggling: will upcoming earnings ignite a comeback?

AI Sentiment: 68/100 Bullish

This score is generated through AI-driven analysis of the article's content.

powered by

Buy AMZN. The setup is clear: AWS is still growing (28% YoY to $37.8B) and operating income is up, but the market is punishing free cash flow after the data-center spend. July 30 earnings are the catalyst to prove ROI is improving while AWS growth holds. Technicals support a near-term bounce (inverted head-and-shoulders, reclaiming 50/100-day MAs) with upside toward $278.

Key Risk: AWS growth slows or margins/ROI disappoint, and free cash flow stays weak despite the $200B+ spend.

Buy NVDA. If AMZN’s earnings confirm AI/data-center momentum, hyperscaler capex expectations rise and the market rotates into the biggest AI compute bottleneck. NVDA is the direct beneficiary of more server/AI training demand tied to AWS and Amazon’s chip/Tranium capacity deals, and it typically re-rates when hyperscaler spending fears fade.

Key Risk: AI demand softens (or hyperscalers delay capex), causing NVDA guidance to miss even if AMZN beats.

- Amazon stock has underperformed the market this year.

- There are concerns about its artificial intelligence spending.

- Focus is on the upcoming financial results, which will come out later this month.

Amazon stock has struggled to keep pace with the broader market this year as investor sentiment toward hyperscalers has cooled. AMZN is up about 8% year to date and just 10% over the past 12 months, lagging many large-cap peers.

However, the stock could regain momentum later this year if investors rotate back into hyperscalers amid renewed optimism about AI spending, cloud growth, and earnings.

Amazon earnings may provide earnings

AMZN stock price has underperformed the market this year as investors remained concerned about its spending and whether it will achieve a return on investment (ROI).

The company has been spending billions of dollars in data centers. It plans to spend over $200 billion this year, a figure that may continue growing as memory, servers, and chip prices surge.

The next key catalyst for the company is its earnings, which are expected to come out on July 30th. These earnings will provide an overview of how its business performed last quarter, and whether its cloud business is still growing.

The last financial results showed that its sales jumped by 17% in the first quarter to $181 billion. Excluding its forex benefits, the company’s sales rose by 15% from the same period last year.

By segment, is international sales rose by 19%, while AWS jumped by 28% to $37.8 billion. Its North America segment jumped by 12% to $104 billion, as retail spending growth continued.

Most notably, despite its strong spending, Amazon’s operating income rose to over $23.9 billion, with AWS leading the pack with $14.2 billion. However, the key blemish in the report was its free cash flow, which plunged to $1.2 billion in the trailing twelve months as it boosted its spending.

There were a few notable statements in the report. For one, the company’s chip business, which is made up of Graviton, Terranium, and Nitro, made $20 billion in annual revenue run rate. It also inked a deal with OpenAI to consumer about 2 GW of Tranium capacity.

Amazon’s growth to continue

The upcoming earnings report is expected to show that revenue jumped by 16.8% in the second quarter to over $195 billion. Notably, the IWS division is expected to grow by about 25% as the company’s market share in the cloud computing sector remains.

For the year, the company’s revenue is expected to grow by 15% to $823 billion, followed by $930 billion next year.

There are signs that the company has become highly overvalued, with the forward price-to-earnings ratio hitting 29. Its multiple is much higher than the sector median of 15.

Most Wall Street analysts remain bullish on Amazon stock. The average price target is $312, implying about 25% upside from the current level. Among the most optimistic forecasts, KeyCorp has a $335 target.

Meanwhile, Wedbush, Citigroup, and Citizens maintain Outperform, Buy, and Market Outperform ratings, respectively, reflecting continued confidence in the company's long-term growth prospects.

READ MORE: Is Big Tech's $725B AI splurge being funded by mass layoffs?

Amazon stock price technical analysis

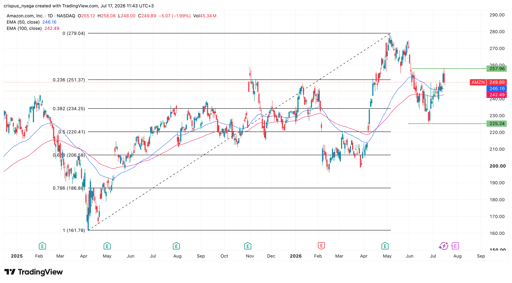

AMZN stock chart | Source: TradingView

The daily chart shows that the AMZN stock has crawled back in the past few days, moving from a low of $225 earlier this month to the current $250. It has already crossed the 50-day and 100-day moving average and formed an inverted head-and-shoulders pattern.

It is also hovering around the 23.6% Fibonacci Retracement level. Therefore, the stock will likely bounce back in the near term as investors start rotating from memory and semiconductor companies to hyperscalers. If this happens, the next key target to watch will be the year-to-date high of $278.

Dow falls 454 points as earnings, Hormuz tensions weigh on Wall Street

Evening digest: Alphabet bond raise, oil jumps as Hormuz risks return

Honeywell Aerospace stock sinks 20% after guidance cut clouds outlook

Figma stock dropped after earnings: here’s why it may rebound soon

AppLovin stock sinks on Q2 earnings: buy the dip or sell the rip?

No results found

Loading articles...

Failed to load articles. Please try again.