Aluminium market faces 3 million tonne hole as ING warns deficit will stay

AI Sentiment: 68/100 Bullish

This score is generated through AI-driven analysis of the article's content.

powered by

Buy LME Aluminium (cash or 3–12 month futures). ING’s core point is a structural deficit: ~3m tonnes of lost production won’t be restored quickly, and even with de-escalation the market stays tight (LME stocks ~314k tonnes, down ~40% YTD). China exports help, but can’t fully offset because output is constrained by the capacity cap and power/permitting limits. This keeps the “geopolitical premium” from fully collapsing while physical tightness supports prices.

Key Risk: A fast, large supply rebound (smelters restart quickly or new capacity comes online) that closes the deficit and rebuilds LME stocks.

Buy aluminium producers with meaningful exposure to tight physical markets (e.g., Rio Tinto, Alcoa). If the market remains in deficit, producers benefit from firmer realized prices and improved contract pricing, while inventory drawdowns support premiums. The thesis is that easing Middle East risk won’t remove the fundamental shortage, so earnings power holds up even as headline risk fades.

Key Risk: Price weakness from a demand shock (industrial slowdown) that overwhelms the supply deficit and forces producers to cut output/discount sales.

- Aluminium deficit of 1.8M tonnes expected this year.

- Fundamentals remain supportive for higher aluminium prices.

- Chinese exports hit a record, but capacity cap limits further growth.

ING Economics warns that the global aluminium market will remain in deficit this year despite easing Middle East tensions, with supply losses of around 3 million tonnes unlikely to be restored quickly.

ING’s Commodities Strategist Ewa Manthey said in a recent report that fundamentals remain supportive for prices, even as geopolitical risks fade.

The signing of a deal between the US and Iran last week has not prompted ING Economics to change its forecasts for aluminium.

Aluminium deficit persists

The signing of a preliminary Memorandum of Understanding between the US and Iran last week, alongside the extension of the ceasefire, has eased concerns over further disruptions to aluminium supply and shipping routes in the Middle East.

ING Economics noted that while the agreement reduces the risk of additional supply losses, it does not materially change the outlook.

“We continue to expect the global aluminium market to remain in deficit this year,” said Ewa Manthey.

Supply disruptions linked to the conflict have already removed an estimated 3 million tonnes of production from the market.

ING forecasts a global aluminium deficit of 1.8 million tonnes in 2026, underpinned by lost capacity that cannot be restored quickly.

Manthey explained that smelters are designed to operate continuously, and restarting idled capacity can take months and require significant investment.

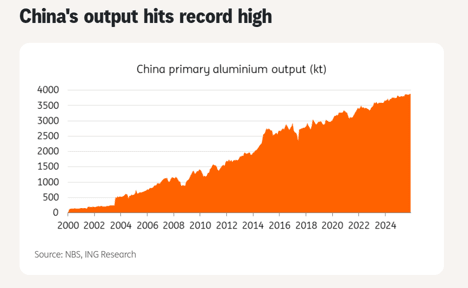

China steps in, but limited scope

Higher Chinese exports have provided some relief. Export volumes rose 15% year‑on‑year in April to 598,000 tonnes and increased a further 16% in May to 630,000 tonnes.

The China Nonferrous Metals Industry Association expects full‑year aluminium product exports to reach a record high in 2026.

The increase has been driven by a widening premium between international and Chinese aluminium prices, encouraging producers to maximize exports.

Weaker domestic demand and elevated inventories have also supported overseas shipments.

China has boosted alumina exports as well, with May shipments rising 36.4% year‑on‑year to 280,000 tonnes.

Yet Manthey cautioned that China’s ability to expand supply further is limited.

Annualized production is already running at 46.7 million tonnes, above the government’s 45 million tonne capacity cap.

“While higher export volumes have helped alleviate some of the tightness in global markets, there appears to be limited scope for a significant increase in Chinese output,” she said.

Indonesia is expected to add 0.5–0.8 million tonnes of aluminium capacity this year, but ING noted that this is well below the estimated 3 million tonnes lost due to the Middle East conflict.

Power and permitting constraints could further limit output.

As a result, incremental supply growth from Indonesia is unlikely to materially alter market balances in the near term.

Prices supported despite easing risks

During the height of the conflict, aluminium prices incorporated a geopolitical premium reflecting the risk of further supply disruptions.

With the ceasefire extended and the US–Iran MoU providing a framework for negotiations, part of this premium is likely to unwind.

However, Manthey stressed that downside risks remain limited. “We continue to see supportive fundamentals for aluminium despite the recent de‑escalation,” she said.

LME aluminium stocks have fallen to around 314,000 tonnes, down almost 40% from the start of the year despite stronger Chinese exports and easing tensions.

Inventories continue to signal tight physical market conditions. ING maintains its aluminium price forecasts of $3,500 per tonne in Q3 and $3,400 per tonne in Q4.

Outlook

The easing of Middle East tensions has reduced immediate risks, but the aluminium market remains structurally tight.

Lost supply will take months to recover, Chinese exports cannot expand indefinitely, and incremental additions from Indonesia are insufficient to close the gap.

The improvement in the geopolitical backdrop reduces the risk of further supply disruptions, but it does not immediately restore lost production. Chinese exports have not been sufficient to rebalance the market.

Gold nears $4,070: has weaker dollar created a rare buy-the-dip setup?

Oil plunges 7%, but Trump’s Iran pause may be setting up crude’s next rebound

Crude oil price tumbles on Hyperliquid as Trump TACOs on planned Iran attacks

Oil prices fall after volatile week, but the real squeeze may still be ahead

Gold slips below the spotlight, but $4,000 may be the real bull signal

No results found

Loading articles...

Failed to load articles. Please try again.