ING resets gold outlook as correction reshapes 2026 trajectory

AI Sentiment: 28/100 Bearish

This score is generated through AI-driven analysis of the article's content.

powered by

ING says ETF demand is less supportive, but central banks added ~244 tonnes in Q1 and 84% expect higher gold reserve shares. If investor flows stay weak, official-sector buying becomes the main floor. Trade: buy/accumulate PHYS (physical gold trust) as a way to own gold exposure while the market is focused on yields and USD.

Key Risk: Central banks slow purchases materially (or sell) just as ETF selling continues, removing the price floor.

ING cut gold forecasts to $4,300 (Q3) and $4,600 (Q4) citing higher real yields and a stronger USD plus weaker ETF demand. That combination keeps pressure on bullion even if geopolitics stays noisy. Trade: sell/short GLD (or reduce long exposure) into continued yield/DXY strength and only expect stabilization from central-bank buying.

Key Risk: The Fed pivots faster than expected and real yields fall sharply, triggering a fresh ETF-led rally that overwhelms central-bank support.

- ING trims Q3 gold forecast to $4,300, Q4 to $4,600.

- ING said gold price correction increasingly difficult to ignore.

- ETF demand weak, central banks remain strong buyers.

ING Economics has reset its gold price forecasts after a sharp correction, acknowledging that higher yields, a stronger US dollar, and weaker investor demand have eroded the bullish momentum that carried the metal earlier this year.

Commodities strategist Ewa Manthey said the downgrade reflects near‑term headwinds but stressed that long‑term structural drivers remain intact.

Forecasts lowered after correction

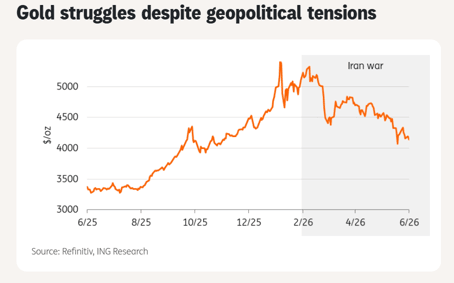

Gold’s rally in the first quarter of 2026 has given way to a steep sell‑off, leaving prices in negative territory for the year.

ING Economics said in its latest release that the correction has become “increasingly difficult to ignore,” forcing a reset in its outlook.

We continue to believe the structural drivers supporting gold remain intact, though the path higher is likely to be slower and more volatile than we previously expected.

The bank now expects gold to average $4,300 per ounce in the third quarter and $4,600 in the fourth quarter, down from earlier forecasts of $4,850 and $5,000, respectively.

The revision marks a significant shift in tone, acknowledging that higher yields and a stronger dollar are likely to weigh on bullion for longer than anticipated.

Manthey explained that the primary driver behind gold’s decline has been a repricing of interest rate expectations.

Following recent Federal Reserve communication, investors have pushed back expectations for monetary easing, driving Treasury yields higher and supporting the dollar.

“This has created a less favourable backdrop for gold, which typically struggles when real yields rise, and the dollar strengthens,” she said.

Investor flows weaken

The weakness has surprised some observers, given ongoing geopolitical uncertainty and continued central bank buying.

Yet markets have shifted focus away from safe‑haven demand toward the implications of tighter financial conditions.

ETF investors, who were instrumental in gold’s rally at the start of the year, have retreated.

Holdings are now about 1.5% below where they began 2026, with profit‑taking particularly evident among North American investors.

Manthey noted that “ETF demand is likely to remain less supportive than it was in 2025,” even as recent inflows suggest selling pressure may be easing.

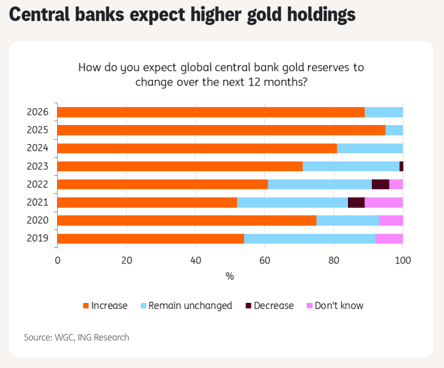

The retreat of speculative investors has left gold more reliant on official sector demand, which has remained robust.

Central banks added around 244 tonnes of gold in the first quarter, with Poland among the largest buyers and China extending its streak to 19 consecutive months.

According to the World Gold Council, 84% of central banks expect gold to account for a larger share of reserves over the next five years.

Manthey said this appetite reflects ongoing diversification efforts and should help stabilize prices despite weaker investor flows.

Silver also downgraded

ING also cut its silver forecasts, reflecting slower growth in solar demand and substitution trends in photovoltaic manufacturing.

The bank now expects silver to average $68 per ounce in Q3 and $74 in Q4, down from $79 and $84.

Manthey said that while silver remains supported by electrification and structural deficits, the pace of gains will be more modest than previously anticipated.

The downgrade underscores how quickly sentiment has shifted in precious metals.

Rising yields and a stronger dollar have eroded investor enthusiasm, while geopolitical tensions have failed to generate the safe‑haven inflows seen in past crises.

For gold, the correction has forced ING to temper expectations, even as long‑term fundamentals remain supportive.

Gold nears $4,070: has weaker dollar created a rare buy-the-dip setup?

Oil plunges 7%, but Trump’s Iran pause may be setting up crude’s next rebound

Crude oil price tumbles on Hyperliquid as Trump TACOs on planned Iran attacks

Oil prices fall after volatile week, but the real squeeze may still be ahead

Gold slips below the spotlight, but $4,000 may be the real bull signal

No results found

Loading articles...

Failed to load articles. Please try again.