Salesforce stock has slumped amid SaaSpocalypse concerns: what next?

AI Sentiment: 22/100 Bearish

This score is generated through AI-driven analysis of the article's content.

powered by

Buy IBM. The article links IBM’s slowdown to customers shifting capex toward servers and memory. That’s exactly the kind of spending that tends to support IBM’s infrastructure-heavy mix versus pure per-seat SaaS. If SaaSpocalypse fears push budgets away from software seats and toward compute, IBM should be relatively insulated and can re-rate as investors rotate from “software replacement” risk to “infrastructure spend” beneficiaries.

Key Risk: Customers cut overall IT budgets (not just software), and IBM’s infrastructure demand weakens enough to overwhelm any capex shift benefit.

Short Salesforce (CRM). The news is a double hit: growth is slowing and the market is pricing “SaaSpocalypse” risk to per-seat software, while Salesforce’s recent growth is partly acquisition-driven (Informatica). Even with Agentforce/data ARR up, the stock is still below key trend levels (50-week EMA, Supertrend, and near the 78.6% fib area), so rallies likely get sold. Valuation looks cheap, but the article flags that metrics are distorted by the Informatica deal—so “bargain” can be a value trap.

Key Risk: Agentforce/data growth re-accelerates fast enough to prove AI agents won’t replace Salesforce’s pricing power, and guidance beats expectations for multiple quarters.

- Salesforce stock has plunged by over 50% from its all-time high.

- It has slumped amid the ongoing SaaSpocalypse concerns.

- Technical analysis suggests that the stock will continue falling.

Salesforce stock has plunged by more than 50% from its December 2024 peak as concerns about its growth outlook have intensified. Its market capitalization has fallen from more than $347 billion to about $136 billion, and the selloff could continue as investors remain concerned about the company's strategy and long-term growth prospects.

Salesforce stock has dropped amid SaaSpocalypse fears

CRM stock has been in a steep decline over the past few years as concerns about its growth have escalated. Recently, the stock has dropped because of the rising SaaSpocalypse fears.

SaaSpocalypse is a relatively new term referring to fears that AI agents will replace traditional software and the “per seat” pricing model. A good example of this is what Starbucks is doing.

According to Bloomberg, the company is now building its own AI-assisted replacement for a Microsoft system that tracks inventory and an IBM solution that manages maintenance. It aims to save the $400 million it spends annually on software.

The fears in the software industry escalated this week after IBM published its financial results. IBM said that its business slowed as customers reprioritized their capital expenditure, redirecting it towards hardware purchases like servers and memory.

Salesforce’s organic growth has been slowing for a while. The most recent results showed that its revenue rose by 13% in the first quarter. While this growth is solid for a company that has been in business for years, it was not organic. Its $11.1 billion revenue included $444 million from Informatica, a company it acquired in a $8 billion deal.

The company has been one of the most acquisitive ones in the US. It has spent billions of dollars acquiring firms like Own Company, Fin, Bluebirds, Tableau, and Slack.

Analysts expect that Salesforce’s business will remain under pressure in the coming months. The average estimate is that its revenue jumped by 10% in the last quarter to $11.32 billion. Its annual revenue is expected to be $46.1 billion, followed by $50.4 billion next year.

Bargain or a value trap?

At face value, there are signs that Salesforce stock has become a bargain. For one, its Non-GAAP forward price-to-earnings ratio has dropped to 11.8, well below the sector median of 24. Its five-year average stands at 24.

Similarly, the forward PEG ratio stands at 0.73, also lower than other companies in the tech industry. The challenge, however, is that these valuation metrics include the extra funds made from its Informatica buyout.

As a result, the company will need more growth catalysts over time. One of this catalysts will be its Agentforce and data segments, whose annual recurring revenue soared to $3.4 billion, a 200% jump. It has deployed over 3.8 billion Agentic Work Units (AWU) across Agentforce and Slack.

READ MORE: Salesforce stock falls after KeyBanc downgrade on AI growth concerns

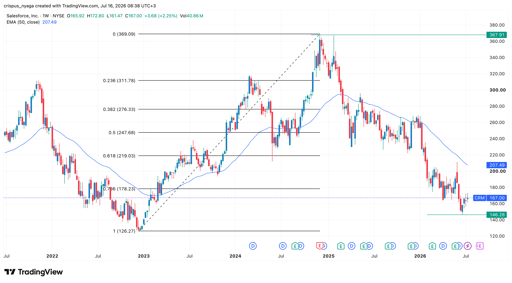

CRM stock technical analysis

Salesforce stock chart | Source: TradingView

The weekly chart shows that the CRM share price has slumped in the past few years, moving from a record high of $367 to a low of $146. It remains below the 50-week Exponential Moving Average (EMA).

The stock has also remained below the Supertrend indicator and the 78.6% Fibonacci Retracement level.

Therefore, the stock will likely remain under pressure in the near term. In this, it may drop and retest the year-to-date low of $146.

In the long-term, however, the stock will likely bounce back as investors buy the dip in software stocks.

Micron stock plunges: Has it topped, or is this a rare buying opportunity?

SanDisk stock is stuck in a bear market: buy the dip or sell the rip?

$10,000 in each of QQQ, TQQQ, and SQQQ 5 years ago: Here's the result

The world's most valuable IPO, SPCX, is now Wall Street's most shorted new stock

London stocks edge lower as geopolitical concerns offset gains in midcaps

No results found

Loading articles...

Failed to load articles. Please try again.