Top reasons Tesla stock price may crash to $350

Tesla stock price has crashed into a technical bear market after slipping by over 20% from its highest level in 2025.

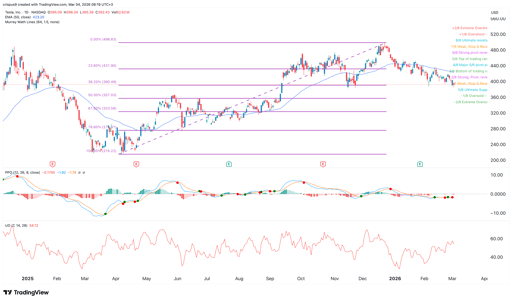

It was trading at $396 on Tuesday, and some key fundamentals and technicals suggest that it may drop to $350 and below in the near term.

Tesla stock price technical analysis points to more downside

The daily timeframe chart shows that the TSLA stock price has crashed in the past few months and is now hovering near its lowest level since November last year.

In contrast, top US indices like the S&P 500 Index and the Dow Jones are hovering near their all-time highs.

Tesla stock price has moved below the 23.6% Fibonacci Retracement level and is now nearing 38.2%. This retracement is drawn by connecting the lowest and highest levels in 2025.

Buy Tesla stock instantly on eToro.

Worse, the stock is about to form a death cross pattern, which happens when the 50-day and 200-day Weighted Moving Averages (WMA) cross each other.

The spread between the two has continued narrowing in the past few days and could happen soon.

Tesla stock has also dropped below the key Supertrend indicator.

It also remains below the Ichimoku cloud, while top oscillators like the Relative Strength Index (RSI) and the MACD have pointed downwards.

Therefore, the most likely Tesla stock price forecast is bearish, with the next key target being $350.

This target is both a psychologically important level and the 50% Fibonacci Retracement.

The bearish Tesla stock outlook will become invalid if it rises above the 23.6% Fibonacci Retracement level at $430.

Tesla is facing stiff competition in Europe and China

Meanwhile, Tesla is losing market share in key markets like Europe and China.

Data released this week showed that Tesla’s new vehicle registrations in the European Union, the UK, and EFTA plunged by 17% in February. It delivered just 8,076 vehicles in these countries.

Tesla’s sales have dropped by a bigger rate in some other countries.

For example, its registrations in the UK tumbled by 57%.

On the other hand, some Chinese brands are doing much better.

A good example of this is BYD, which delivered 18,242 vehicles in the region, a 165% annual increase. BYD is benefiting from the fact that its vehicles have advanced features and normally cost less than Tesla's.

China is also becoming a challenge as top firms like BYD and Nio gain market share.

Pivot to AI and robotics will be tough

Meanwhile, there is a likelihood that the company’s pivot to key industries like artificial intelligence and robotics will be tough.

For example, the company aims to deploy robotaxi services, which Elon Musk said will be the largest asset value increase in human history.

However, launching these vehicles will be tough. Indeed, a Polymarket contract with over $67,000 in assets places the odds of Tesla launching its robotaxi service in California by June have dropped to 23%.

The same is true with the launch of Optimus, its robots. While robotics is a big market, it is unclear whether Tesla will gain market share as the industry has some major market leaders like ABB and Fanuk.

All these challenges are happening despite Tesla being one of the most overvalued companies in the United States.

Data shows that the company has a forward PE ratio of 194, much higher than the sector median of 15. The S&P 500 Index has a forward PE ratio of 22.

It is common for some quality companies with a large and growing market share to have a premium valuation.

A good example of this is Nvidia, which has a forward PE ratio of 40. Its valuation is understandable as the company has over 50% in annual growth.

In Tesla’s case, its revenue growth has stalled, market share is diminishing, and its future products, like robo taxis and Optimus, are unproven.

DRAM ETF braces for key Samsung, SK Hynix, Kioxia, Seagate earnings

Could SpaceX stock fall to $100? Morgan Stanley says it means a zero AI valuation

Bloom Energy stock rises ahead of earnings: will the gains hold?

AI has changed how Wall Street values companies

Top 3 catalysts for the S&P 500 and Nasdaq 100 indices this week

No results found

Loading articles...

Failed to load articles. Please try again.