Lloyds share price is up 47% in 12 months: why it may soar to 141p

AI Sentiment: 82/100 Bullish

This score is generated through AI-driven analysis of the article's content.

powered by

Buy LLOY. The news points to a clean earnings engine: net interest income +8% in Q1, other income +11%, and costs/remediation down to £2.48bn. Analysts also see costs rising slowly while net income grows (20.2bn this year to 22.9bn by 2028), plus rising dividends (3.65p to 6.12p by 2028). The chart setup supports momentum: above the 100-day MA, Supertrend, and Ichimoku clouds, with a cup-and-handle target near 141p.

Key Risk: A sharp fall in interest rates or credit losses that crush net interest income and force higher provisions, wiping out the earnings and dividend growth story.

Buy a UK bank momentum basket with LLOY as the core (e.g., iShares MSCI UK Financials ETF (ISF) or similar UK financials exposure). The thesis is that improving UK bank profitability (higher net interest margins + cost discipline) is a sector-wide rerating, and the article’s bullish technicals for LLOY suggest flows will keep rotating into UK financials.

Key Risk: A sector-wide shock—regulatory capital pressure or a UK credit downturn—that hits multiple banks at once, not just Lloyds.

- Lloyds share price has jumped sharply in the past few months.

- The company will likely continue doing well in the coming years.

- Technicals suggest that it may blast to 141p over time.

Lloyds share price has pulled back over the past few days, falling from its year-to-date high of 116p to the current 112.10p. Although the stock has surged by 47% over the past 12 months, there are several reasons why it could continue rising in the foreseeable future.

Analysts are optimistic about Lloyds Bank growth

Lloyds Bank is a top British banking group that owns businesses like Scottish Widows, Bank of Scotland, MBNA, and Bank of Scotland. Combined, its brands have over 28 million customers.

The company’s business has done well in the past few years, even as the UK economy has stagnated. One reason for this is that interest rates have remained at an elevated level in the past few years. The BoE hiked rates after COVID to combat inflation, which helped banks grow their net interest margin.

At the same time, the company has embraced technology that has helped it to cut costs. A good example of this is its mobile banking solutions, which have led to more transactions over time.

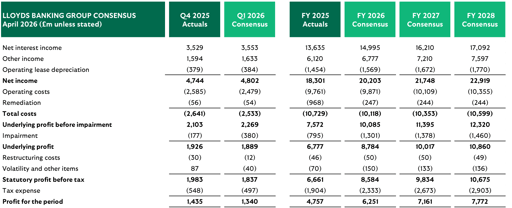

The most recent results showed that the net interest income rose by 8% to £3.56 billion in the first quarter. Its other income rose by 11% to £1.6 billion.

The company has also reduced its operational expenses in the past few months. Its Q1 costs and remediation dropped to £2.48 billion from £2.64 billion in the same period last year.

Analysts are optimistic that its growth will continue in the coming years. For example, data shows that analysts expect that its net income will be £20.2 billion this year, followed by £21.7 billion next year and £22.9 billion in 2028.

Notably, these analysts expect that its total costs will grow at a slow pace over time. Total costs are expected to come in at £10.11 billion this year, followed by £10.35 billion next year and £10.5 billion in the following year.

As a result, the annual revenue will jump from £4.75 billion last year to £7.78 billion in 2028. Historically, Lloyds tends to do better than estimates, meaning that its performance will be higher than these figures.

Lloyds forward estimates | Source: Lloyds

At the same the company continues returning funds to its shareholders. Its dividend per share has jumped from 2p in 2021 to 3.65p last year, and analysts expect that the figure will hit 6.12p in 2028. It has done that by using its free cash flow and by reducing its CET1 ratio.

Technicals suggest that Lloyds share price will continue rising

LLOY stock chart | Source: TradingView

Meanwhile, there are signs that the Lloyds stock price has formed a cup-and-handle-like pattern on the daily chart. The recent retreat is part of the formation of the handle section.

This cup has a depth of 23%. Measuring the same distance from the cup’s upper side, suggests that the stock will eventually jump to 141p, which is about 26% from the current level.

Other technicals are also highly bullish for the stock. It has remained above the 100-day moving average and the Supertrend indicator. Also, it remains above the Supertrend and the Ichimoku clouds, pointing to more gains.

Lucid stock jumps 20% as Saudi billionaire prince buys the dip: what next?

Amazon stock could swing $15 after Q2 earnings: what will drive the move?

Bloom Energy stock surges 10% after record quarter as AI demand fuels growth

Why is Ford stock surging despite a $1.3 billion loss?

European shares edge higher as miners and energy stocks lead gains

No results found

Loading articles...

Failed to load articles. Please try again.